Managing Your Money: The 50/30/20 Rule

Key Takeaways

- The 50/30/20 rule is a simple and effective framework for managing your money, dividing your income into three categories: needs, wants, and savings.

- This method helps you balance essential expenses with lifestyle spending while building a habit of consistent saving.

- It is a guideline; you can adjust the percentages based on your personal financial situation and life stage.

- For Singaporeans, understanding how to budget effectively is crucial given the high cost of living and easy access to credit and BNPL services.

In Singapore, managing personal finances can feel like an uphill battle. With the rising cost of living and inflation impacting everything from groceries to utilities, many of us find ourselves wondering, “how much should I save per month?” Furthermore, it’s easy to get caught up in spending, especially on things we don’t really need.

Likewise, the convenience of modern payment options, such as credit cards and Buy Now, Pay Later (BNPL) services, has made it simpler than ever to overspend on non-essential purchases. Without a clear plan, our income can disappear before any part of it goes toward funding our future goals. This is where structured budgeting can help.

One of the most popular and beginner-friendly frameworks for how to budget your salary is the 50/30/20 rule. It is a straightforward method that can help most middle-income earners take control of their finances. This article will explain how the 50-30-20 rule works and, more importantly, how you can adapt it to suit your unique financial situation in Singapore, setting you on the path toward financial freedom.

What Is the 50/30/20 Budgeting Rule?

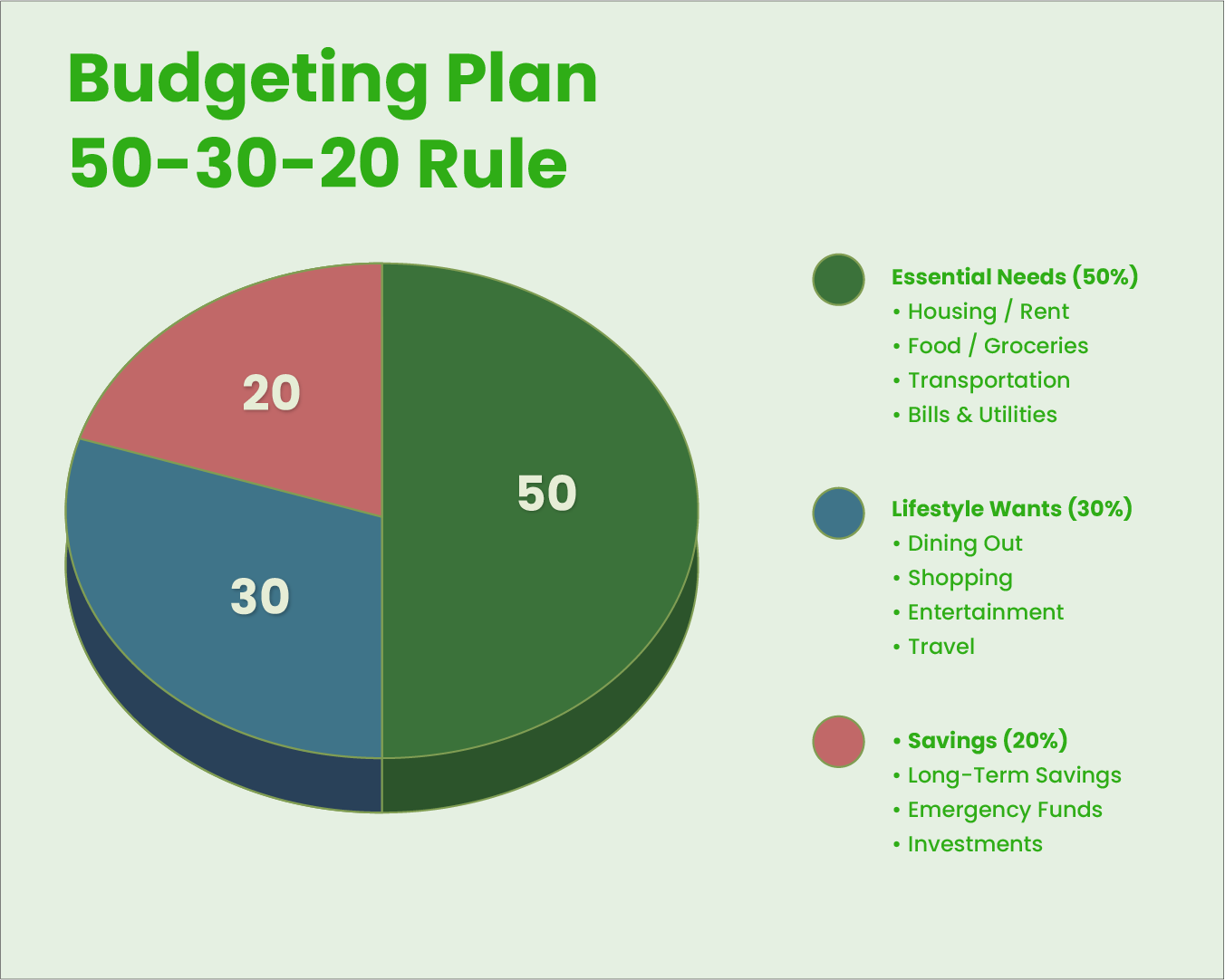

The 50/30/20 rule is a simple, intuitive guideline for budgeting that helps you allocate your after-tax income into three primary buckets: needs, wants, and savings.

Popularised by Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan,” its beauty lies in its simplicity. Instead of tracking every single cent, this framework helps you build good financial habits.

The core principle is to balance financial discipline with lifestyle spending. It helps you avoid overspending, build consistent savings habits, and ensures you are actively working towards your long-term financial objectives, rather than just letting your money slip through your fingers.

50%: Needs

These are your essential expenses—the non-negotiable costs required for daily living, the things you must pay for, regardless of your lifestyle. According to the 50/30/20 rule, up to half of your take-home pay should cover these necessities. In Singapore, common examples include:

- Housing: Mortgage or rent payments.

- Utilities: Bills for electricity, water, and gas.

- Groceries: Essential household staples like food and cleaning products.

- Transport: Basic public transport fares (MRT, bus).

- Insurance: Essential insurance premiums (e.g., MediShield Life, Integrated Shield Plans).

- Loan Repayments: Any debt, such as student loans or credit cards.

30%: Wants

These are the discretionary spending that enhances your lifestyle but aren’t essential for survival. A good rule of thumb for distinguishing a “want” from a “need” is to consider if you could have avoided the expense. For example, taking a taxi when the MRT is a viable option turns that fare into a “want”. Common examples include:

- Dining Out: Meals at cafes and restaurants, or even frequent bubble tea runs!

- Shopping: Purchasing fashion items, the latest gadgets, or luxury goods.

- Entertainment: Going to the cinema, watching live performances, or attending concerts.

- Travel: Holidays and weekend getaways.

- Hobbies and Leisure: Spending on recreational activities, gym memberships, or subscription services like Netflix or Spotify.

20%: Savings

The final 20% of your income should be directed toward your financial future. Although named “savings”, this category also includes what you do with your savings, such as investing it to help your money grow over time. It is the foundation for achieving long-term goals while building a safety net. This portion can be allocated to:

- Emergency Fund: Setting aside 3–6 months’ worth of living expenses in a high-liquidity account for unexpected events like job loss or medical emergencies.

- Retirement Planning: Making voluntary contributions to your CPF or Supplementary Retirement Scheme (SRS) for tax relief and long-term growth.

- Long-Term Goals: Saving for a down payment on a house, your children’s education, or other significant future expenses.

- Investments: Putting money into assets that can generate returns, such as stocks, Exchange-Traded Funds (ETFs), or unit trusts, to outpace inflation or generate passive income.

A crucial point to remember is that leaving your money in a low-interest savings account or as idle cash may erode its value over time due to inflation.

In Singapore, the average inflation rate over the past 30 years has been around 1.73%, underscoring the importance of investing to preserve your purchasing power.

For context, according to the Department of Statistics Singapore, the personal savings rate was 36.4% in the last quarter of 2025. While this is higher than the rule’s 20% suggestion, it indicates a strong culture of saving in Singapore, though this figure includes mandatory CPF contributions and varies greatly from person to person.

Who Should Use the 50/30/20 Budgeting Rule?

This budgeting method is perfect for anyone looking for a simple, structured way to manage their money without getting bogged down by complex spreadsheets. It lacks nuance as it’s a generalised rule, but it’s well-suited for:

✅ Fresh Graduates: Those starting their careers and building their savings from scratch.

✅ Individuals Struggling to Save: People who tend to discover their money somehow runs out before the end of the month.

✅ Anyone Needing a Simple System: Those who want a clear and easy-to-follow money management plan.

Benefits of the 50/30/20 Budget Rule

Adopting this framework offers several key advantages that contribute to long-term financial well-being:

- Simple and Easy to Follow: It provides a clear, high-level structure without requiring you to track every dollar obsessively.

- Improves Money Management: By categorising your expenses, you increase your awareness of your spending habits, which helps you identify where you might be overspending.

- Encourages Consistent Saving: By treating savings as a non-negotiable 20% of your income, it makes building your financial future a priority, not an afterthought.

- Supports Long-Term Financial Goals: The dedicated savings bucket ensures you are consistently working towards major life goals such as retirement or a housing down payment.

- Provides Financial Safety Buffer: The emphasis on savings helps you build an emergency fund that serves as a crucial safety net for unexpected life events.

How to Apply the 50/30/20 Rule to Your Budget

Implementing this rule is straightforward: start with understanding your own cash flow.

Step 1: Track Your Expenses

The first step is to gain a clear picture of your monthly income and expenses. Track every dollar you spend for a month or two to see where your money is actually going. This will make it much easier to categorise your expenses into needs, wants, and savings.

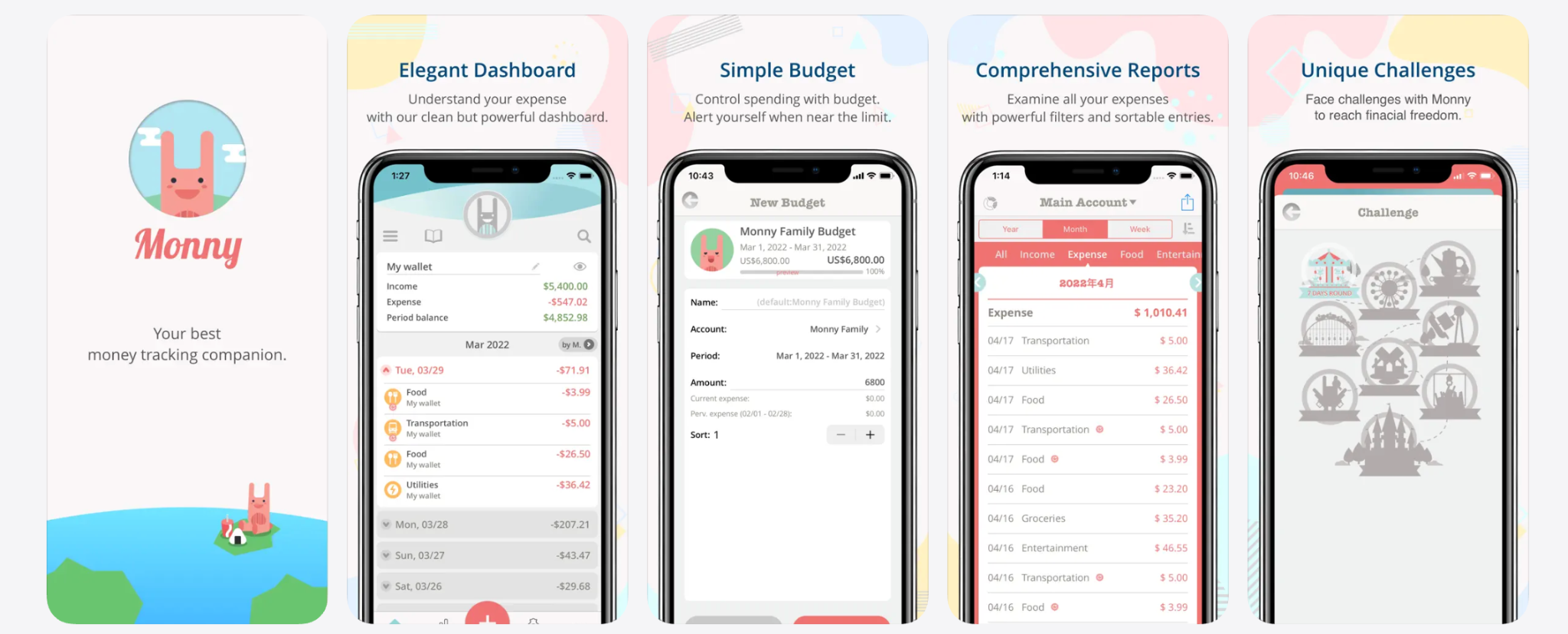

There are several useful budgeting apps available in Singapore to help with this, such as:

Photo Credit: Monny App

- Monny App: A popular free app that helps you track expenses and create budgets.

- Spendee: An all-in-one personal finance manager that tracks your spending. The application converts your data into clear, easy-to-understand visual formats that give you instant clarity on your financial standing.

Step 2: Adjust As Needed

Remember—the 50/30/20 rule is a guideline, not a strict financial mandate! You can and should make tweaks based on your personal life stage and financial goals.

For example, if your essential expenses are lower because you are still living with your parents, you can allocate more than 20% towards savings or investments. Conversely, if you are going through a major life event like getting married, buying a home, or starting a family, your “needs” might temporarily exceed 50%.

The key is to be aware of these shifts and adjust your spending in other categories to maintain overall control of your finances.

Step 3: Prioritise Your Essential Expenses

Rule number one: Pay yourself first.

When you receive your salary, it’s crucial to prioritise covering your essential expenses first. This means ensuring you have enough set aside for your mortgage or rent, utilities, groceries, and transport.

These are the costs that keep your life running smoothly and are generally predictable from month to month. Allocating funds to these essentials first can also help prevent the financial stress of falling behind on bills.

Step 4: Stay Consistent With Your Budget

Consistency is the secret ingredient that makes the 50/30/20 rule work. By following the same budgeting approach each month, you build a powerful financial habit. This consistency helps you avoid going over budget and allows you to see your progress toward your goals month after month. Eventually, if you have a sound investment strategy, you could also achieve financial freedom.

Conclusion

The 50/30/20 rule is more than just a budgeting tool; it is a simple yet powerful framework to build lifelong financial discipline. Its objective is to help you develop good money habits by providing a clear and balanced structure for your income. By ensuring you cover your needs, enjoy your wants responsibly, and consistently pay your future self first, you create a solid foundation for long-term financial well-being.

While this method provides an excellent starting point for managing your cash flow, life often throws unexpected expenses our way. Whether it’s an unforeseen medical bill, urgent home repair, or a need to consolidate high-interest debt, sometimes you need a little extra help to stay on track.

For those moments, understanding your financial options is key. You can learn more about different types of borrowing in our guide on secured vs unsecured loans. And when you are ready to explore a financial solution that fits your needs, feel free to check out our personal loan page or apply now to see how we can help you navigate your financial journey with confidence. For your travel needs, check out our best multi-currency cards and travel cards.