Key Takeaways

- Chocolate Finance offers 2% p.a. returns on your first S$20,000, 1.8% p.a. on your next S$80,000, and up to $1.8% on any amount above that. Returns are credited daily with no lock-ins.

- You can also make USD deposits and enjoy up to 4.1% p.a. in returns.

- Your funds at Chocolate Finance are invested in a diversified portfolio of money market and short-duration bond funds designed to generate returns while maintaining low risk.

- You also get a free Chocolate Finance Visa Debit Card that earns 1 Max Miles per S$1 spent, with competitive Visa exchange rates and no foreign transaction fees.

- Funds invested in Chocolate Finance aren’t insured by SDIC. That said, they’re held separately in custodian accounts, ensuring compliance with MAS regulations and framework.

With traditional savings accounts offering modest interest rates, you may be looking for an investment that can provide potentially higher returns on idle cash. One such platform is Chocolate Finance, a Singapore-based fintech that combines cash management features with a rewards-earning debit card.

Chocolate Finance currently offers returns of up to 2% p.a. for SGD balances and up to 4.1% p.a. for USD balances, with daily credited returns, no hoops to jump through, and no lock-in periods.

In our Chocolate Finance review, we’ll cover what Chocolate Finance is, how it works, the Chocolate Finance Card, and how it compares to other similar investments and multi-currency cards.

Chocolate Finance Overview

| Feature | Details |

| SGD returns | First S$20,000: 2% p.a. Next S$80,000: 1.8% p.a. Above S$100,000: up to 1.8% p.a. |

| USD returns | First US$20,000: 4.1% p.a. Next US$80,000: 3.8% p.a. Above US$100,000: up to 3.8% p.a. |

| Returns credited | Daily |

| Lock-in period | None |

| Minimum balance | None |

| Maximum balance | None |

| Withdrawal timeline | Typically up to three business days |

| SDIC insured? | No |

| MAS regulated? | Yes |

| Chocolate Finance Debit Card earn rate | 1 Max Mile per S$1 spent on the first S$1,000 per month; 0.4 Max Miles per S$1 thereafter |

| Foreign transaction (FX) fees | None |

| Exchange rates | Visa rates with no hidden markup |

What Is Chocolate Finance?

Chocolate Finance is a Singapore-based fintech platform operated by Chocfin Pte. Ltd.

It’s a fund management company licensed by the Monetary Authority of Singapore (MAS) and holds a Capital Markets Services (CMS) licence.

The platform is designed to help users earn potentially higher returns on their spare cash compared to conventional bank savings accounts. Think of it as a hybrid low-risk cash management account and high-yield savings account.

Users can deposit funds in SGD and USD, with rates of up to 2% p.a. on SGD balances and up to 4.1% p.a. on USD balances.

Key features of Chocolate Finance include:

- Daily credited returns

- No lock-in periods

- No penalties for withdrawals

- No complicated requirements to earn interest, such as salary crediting or minimum spending requirements

Opening an account is free, and Chocolate Finance doesn’t charge any monthly or withdrawal fees.

Additionally, every account holder will receive the Chocolate Finance Visa Debit Card, which promises 1 Max Mile per S$1 spent on the first S$1,000 spent each calendar month, competitive Visa exchange rates, and no foreign transaction fees.

How Does Chocolate Finance Work?

As Chocolate Finance isn’t a bank, it doesn’t offer a savings account.

Instead, it invests your money in a carefully curated and diversified portfolio of money market and short-term bond funds.

The underlying funds currently include:

- Dimensional Short-Term Investment Grade Fixed Income SGD Fund (DSF)

- UOBAM United SGD Fund (USF)

- Fullerton Short Term interest rate SGD Fund (FST)

- LionGlobal Short Duration Bond SGD Fund (LGF)

- Amova Short Term Bond Fund (NST)

According to their FAQ, the exact portfolio composition may change over time at the fund manager’s discretion. You can see information about each fund and its allocation percentage in the Chocolate Finance app.

It’s also worth noting that your capital and returns aren’t guaranteed as they’re exposed to market fluctuations.

Since Chocolate Finance isn’t a bank, your deposits aren’t covered by the Singapore Deposit Insurance Corporation (SDIC).

For the uninitiated, the SDIC basically protects your Singapore-dollar deposits in a bank up to S$100,000 per depositor per bank. This means that your money in a bank will be insured up to S$100,000 should the bank or financial institution fail. All banks and finance companies in Singapore are required to be members of SDIC.

Chocolate Finance Interest Rate

Under Chocolate Finance’s Chocolate Top-Up Programme, Chocolate Finance offers promotional interest rates on both SGD and USD balances during the qualifying period.

For SGD balances, you’ll earn:

- 2% p.a. on your first S$20,000

- 1.8% p.a. on your next S$80,000

- Up to 1.8% p.a. on any amount above that

For USD balances, the Chocolate Finance interest rates are:

- 4.1% p.a. on your first US$20,000

- 3.8% p.a. on your next US$80,000

- Up to 3.8% p.a. on any amount above that

You can add or withdraw USD directly to/from your bank account, or convert between SGD and USD instantly on the Chocolate Finance app. Note that there’s a fixed FX fee of 0.25% to 0.50% when converting from SGD to USD.

What’s the draw here? Well, if the underlying portfolio underperforms, Chocolate Finance will top up the shortfall so users can continue to enjoy the promotional rate!

The qualifying period for the Chocolate Top-Up Programme runs till 30 September 2026, or until the assets under management (AUM) reach S$1.5 billion—whichever comes first.

It’s important to note that while Chocolate Finance is relatively low-risk, returns and capital aren’t guaranteed, and the firm may change the qualifying period or adjust rates at any time.

Chocolate Finance vs Other Similar Investments

Since Chocolate Finance markets itself as an investment instrument for you to park your spare cash, here’s how it compares to other similar investments that have a similar proposition, such as low-risk cash management accounts, Singapore Savings Bonds (SSBs), Singapore Treasury Bills (T-bills), and fixed deposits.

| Provider | Yield (p.a.) | Minimum deposit | Criteria to earn rate | Source of funds |

| Chocolate Finance | 2% | N/A | No criteria, no minimums, no maximums | Cash |

| Syfe Cash+ Guaranteed | 1.2% to 3.45% | N/A | No criteria, no minimum, no maximums | Cash or SRS |

| T-bills (6-month) | 1.48% (BS26111H) | S$1,000 | Minimum investment of S$1,000 and subsequent investments in multiples of S$1,000 | Cash, SRS, or CPF |

| SSBs | 2.11% (SBJUL26 GX26070F) | S$500 | Minimum investment of S$500 and subsequent investments in multiples of S$500, up to S$200,000 | Cash or SRS |

| Fixed deposits (1 year) | 1.50% (RHB) | S$20,000 | Minimum deposit of S$20,000 | Cash, SRS, or CPF |

Source: Chocolate Finance and additional research

What Happened to Chocolate Finance in 2025?

In March 2025, a couple of financial influencers encouraged their followers to withdraw their funds from Chocolate Finance. Their posts went viral, and panic-stricken customers began withdrawing money from their accounts, believing that a bank run was imminent.

As a result, the sudden surge in customer withdrawal requests placed significant pressure on Chocolate Finance’s instant withdrawal structure.

In response, the company temporarily suspended its instant withdrawal feature and reverted to a standard withdrawal process, which required time to liquidate the underlying investments and transfer the funds back to customers.

Additionally, the situation was further exacerbated by Chocolate Finance’s abrupt decision to block the Chocolate Finance Debit Card for bill payments, including those made through AXS. Chocolate Finance claimed that this was because users were exploiting the card’s feature to maximise miles, making the rewards programme unsustainable.

Furthermore, the company initially claimed that AXS had requested its suspension. But AXS clarified that Chocolate Finance had initiated the removal, leading to further backlash and concerns about a lack of transparency in communication.

All in all, over S$500 million in net withdrawals were made in over two weeks, slashing Chocolate Finance’s AUM by nearly 40%. MAS even had to step in to publicly confirm that customer funds were safe and securely segregated in ringfenced accounts.

While the company confirmed that all withdrawal requests submitted during the period were honoured in full, this incident dealt a blow to consumer confidence in the platform.

Is Chocolate Finance Safe?

The short answer is that Chocolate Finance is still safe. However, it’s important to understand that Chocolate Finance isn’t a bank and does not hold a banking licence.

As a result:

- Your deposits aren’t insured by SDIC

- Capital and returns aren’t guaranteed as they’re exposed to market fluctuations

- The Chocolate Top-Up Programme promo isn’t indefinite

- Withdrawals may not be immediate

However:

- It’s regulated by MAS and holds a CMS licence

- Funds are held in custodian accounts such as HSBC, Citibank, State Street, and BNP Paribas, which are separate from Chocolate Finance’s own accounts

- This helps to safeguard customers’ funds if Chocolate Finance is acquired, restructured, or ceases operations

- Chocolate Finance also implements security features such as Singpass MyInfo, real-time alerts, two-factor authentication (2FA), and more

Before parking your funds with Chocolate Finance, it’s important to understand the risks and weigh the pros and cons.

How to Add Money to Your Chocolate Finance Account

You can add money to your Chocolate Finance account from the Chocolate Finance app home page by tapping “add money”. There are three options to top up your account:

- One-time bank transfer: make a one-time bank transfer using your bank account by logging into your chosen bank account and using your Chocolate account details to make a transfer

- Link your bank account via eGIRO for future fast transfers, or schedule regular top-ups

- PayNow QR code: save or screenshot the QR code and use your bank app to make a PayNow transfer

Singapore FAST and PayNow transfers are typically instant; processing may take a few minutes.

Chocolate Finance Withdrawals

Because funds are invested rather than held as cash deposits, withdrawals may take longer to process compared to traditional bank savings accounts.

While most withdrawals can be processed the same day, some may take up to three business days.

Furthermore, if you’ve recently added funds, converted to or from USD or made multiple transactions on withdrawals, it could take up to seven business days for Chocolate Finance to liquidate the underlying investments before transferring the funds to you.

That said, the good news is that:

- There are no withdrawal penalties

- No lock-in periods

- Funds can be withdrawn at any time

You can make withdrawals from your Chocolate Finance account via a FAST bank transfer. Here’s how:

- Tap “withdraw” on the Chocolate Finance app homepage

- Enter the amount you want to withdraw and swipe to confirm

- Withdrawals usually take three to six business days, or up to eight business days if you’re making more than one withdrawal, recently added money, or converted to/from USD

Chocolate Finance Visa Debit Card

Every Chocolate Finance account comes with a free Chocolate Finance Debit Card. To use the card, you’ll need to deposit funds into your Chocolate Finance account.

Through a partnership with HeyMax, the Chocolate Finance Card allows you to earn 1 Max Mile for every S$1 spent.

Earned Max Miles never expire, and can be transferred for points or miles with over 30 airline and hotel loyalty programmes at a 1:1 ratio. These include:

- Asia Miles

- Accor Live Limitless

- Etihad Guest

- EVA Air Infinity MileageLands

- IHG One Rewards

- Qatar Privilege Club

- Qantas Frequent Flyer

- Shangri-La Circle

- THAI Royal Orchid Plus

- Turkish Miles&Smiles

While 1 mile per dollar (mpd) isn’t particularly eye-catching (considering that some credit cards offer 4 mpd or more), where this card truly shines is that you can earn miles on expenses that are typically excluded from credit card rewards, such as:

- Hospital bills

- Government services

- Insurance premiums

- Car parking

- Charitable donations, and

- Education payments

Note that AXS bill payments have been excluded since 5 March 2025.

On top of this, the Chocolate Finance card offers competitive Visa exchange rates with no FX or foreign currency conversion (FCY) fees. For context, credit cards typically charge 3% or more in foreign transaction fees, on top of their lousier exchange rates.

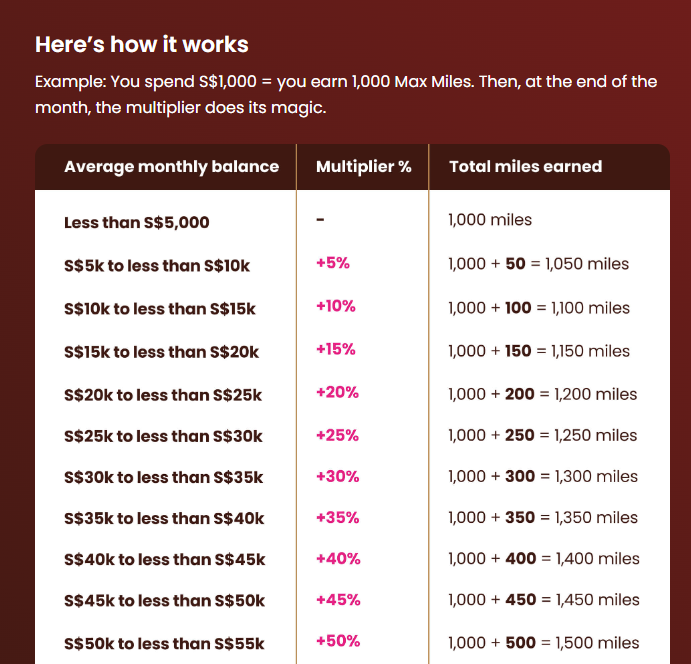

Miles Multiplier

Chocolate Finance also introduced a Miles Multiplier feature, in which higher average account balances can boost the number of miles earned on spending.

Benefits of the Chocolate Finance Visa Debit Card:

- 1 Max Mile per S$1 spent on first S$1,000 monthly spend; 0.4 Max Miles per S$1 thereafter

- No FCY fee

- Competitive Visa exchange rates with no markups

- Earn Max miles on bill payments (capped at S$100 per calendar month)

- No annual fee

- No minimum spend

- No minimum account balance

- Google Pay support, and can be used wherever Visa is accepted

Benefits of the Chocolate Finance Visa Debit Card

- Limited currency support (can only hold balances in SGD and USD)

- Top-ups can only be made in SGD

- Weekday fee of 0.25% or a weekend charge of 0.50% for in-app SGD to USD conversions

- Funds are deducted from your balance. If an unauthorised transaction occurs, it can be hard to recover the funds compared to a credit card

- Bill payments rewards are capped at 100 Max miles monthly

- No ATM withdrawals

Chocolate Finance Visa Debit Card vs Wise vs YouTrip vs Revolut

With very few exclusions, no FCY fee and competitive exchange rates, the Chocolate Finance Debit Card is a solid card for overseas spending. Here’s how it compares against popular multi-currency cards: Wise, Revolut, and YouTrip.

| Feature | Chocolate Finance | Wise | Revolut | YouTrip |

| Interest on balances | Yes | Yes, with Wise Interest (but with an annual fee) | Selected plans | No |

| Supported currencies | SGD and USD | 40+ | 30+ | 12 |

| Exchange rate | Visa exchange rate | Mid-market rate | Own variable rate | Mid-market rate |

| Overseas ATM withdrawals | No | Yes | Yes | Yes |

| FX fee | No | No | 1% on weekends (Standard plan only) | No |

| FCY fee | No | From 0.26% | 0.5% to 1% | No |

| Rewards | 1 Max Miles per S$1 spent | None | Up to 5% cashback | Occasional promotions |

| Google Pay and Apple Pay support? | Google wallet only (for now) | Yes | Yes | Yes |

Verdict: Is Chocolate Finance Suitable for You?

Overall, Chocolate Finance can be a compelling option for users who want to earn returns on idle cash with no lock-ins, daily credited earnings, and no fees.

Moreover, the Chocolate Debit Card lets you earn miles on payments typically excluded by credit cards, while enjoying competitive foreign exchange rates!

Just remember that your capital is exposed to investment risk.

Before depositing large sums, make sure you understand how the platform works, the risks involved, and whether its features align with your financial goals.

Chocolate Finance may be suitable for:

- Users looking to earn returns on idle SGD or USD balances

- Investors who don’t want to jump through hoops such as salary crediting or card spending to earn interest

- Travellers who want a card with competitive FX rates

- Users who want to maximise miles on transactions that don’t typically earn rewards on other credit cards, such as bill payments and government services

It may not be suitable for:

- Users who want SDIC-insured deposits

- Those who want instant access to their emergency funds

- Investors who want guaranteed returns